ESOPs in the Netherlands: from dry tax to something much more usable!

If you spend any time around Dutch venture-backed companies, one pattern comes up quickly: equity is a necessary part of the deal, but tax makes it harder to work with than it should be. That is not because founders or boards misunderstand incentives, but because the tax system so far has not really been designed with early-stage companies in mind.

The proposed Startup and Scaleup Tax Incentive Act is an attempt to correct that. And for ESOPs specifically, it does so by removing two specific frictions that kept coming back in practice: early timing (dry income tax) and rate (full employment rate). We did a deep dive in this Webinar, which we give an Executive Summary on below:

Why timing mattered more than anything else

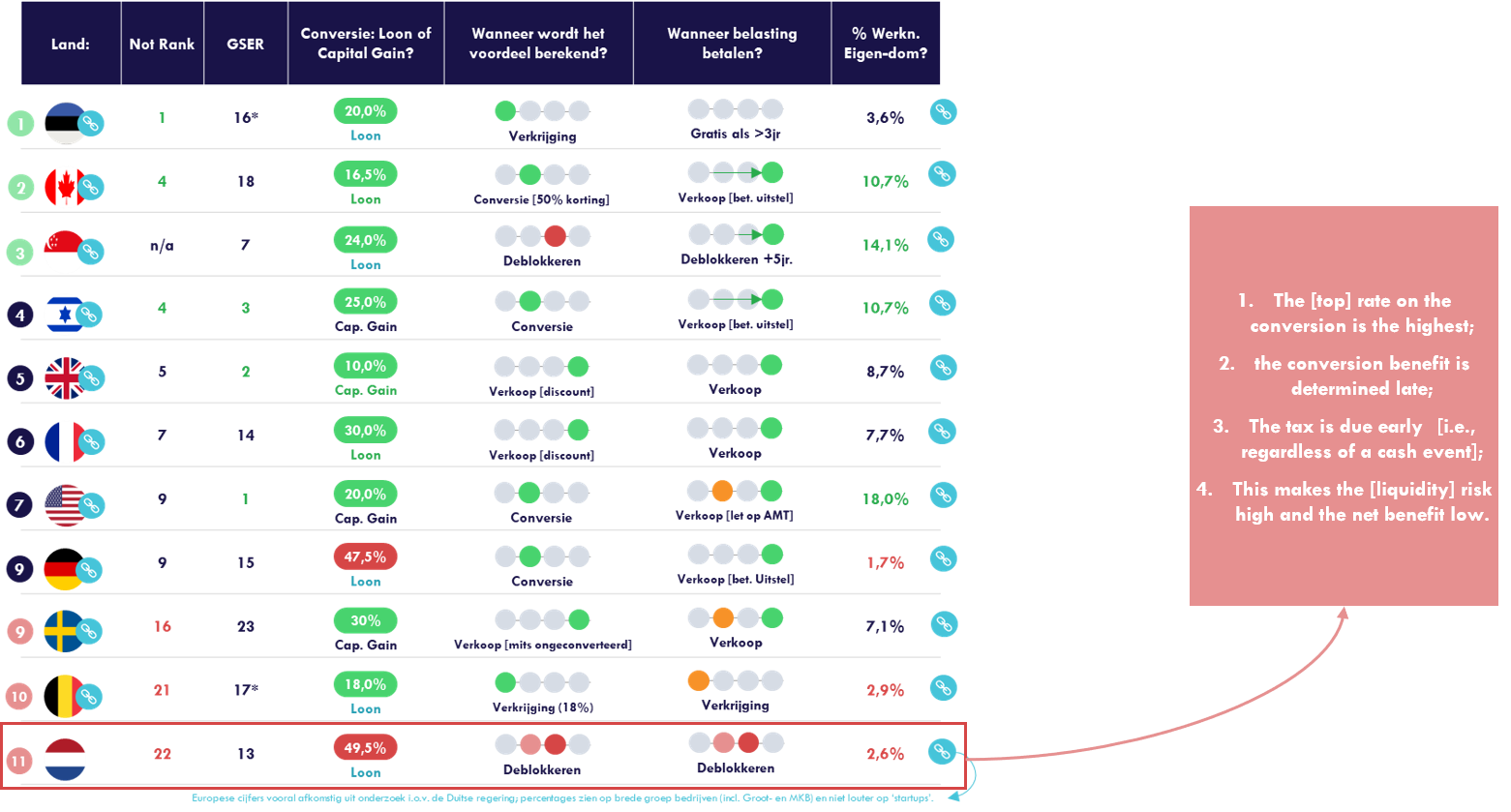

Under the existing rules, the core issue is not that equit-through-ESOPs is taxed (that is unavoidable) but when it is taxed. As opposed to surrounding countries, the Netherlands taxes the ESOP either upon its conversion to shares or when the so acquired share become tradeable (lock-up ends), with the difference between the ESOP’s strike price and the Fair Market Value of the underlying shares (the in the money amount) being identified as a wage-in-kind benefit. So: the rate is full employment rate (up to 49,5%) and there is no organic cash link in the tax trigger. The result was a relatively unfavorable Reward on Risk, as evidenced by a low ranking in Index Ventures’ Not Optional Ranking.

In a typical Dutch setup, this means that an employee could end up with a tax bill at the point the shares become tradable, so even if no sale takes place. On paper, the logic is understandable: once a share is transferable, there is at least a theoretical path to liquidity. In reality, that line is too early. There is usually no market, and very often contractual limitations on selling.

For more on that existing / non-startupregime, check out this primer:

The result is a familiar “dry tax” problem; employees take risk by accepting equity (and uncertain equity at that) over cash, but are asked to pay tax before their risk has converted even into cash. For listed stock, this is mostly manageable as the shares can be ‘sold for cover’. But with startup equity, that’s generally impossible as the equity is subject to lockups and other statutory limitations, for instance because the company wants to avoid ‘dead equity’.

And in that regards, there is a second, more subtle effect; if the tax trigger sits at the moment the shares ‘unlock’, employees may *have* to sell at that point, simply to fund the tax bill. That triggers tax-induced early disposals, which is rarely aligned with how value is created in venture-backed companies where the real upside tends to sit in the ‘heavy tail’ further down the line, nor with the idea behind ESOPs, to reward and retain.

The high tax rate also mattered, especially in cross-border hiring

On top of the timing issue though, the Dutch tax rate also did not help; gains realised as part of the ESOP were taxed in box 1 at rates up to 49.5% whereas in most competing jurisdictions (like Germany, France, the United Kingdom and the United States), employees generally pay later *and* pay less. The combined effect is that the same equity package produces materially different net returns and, notably, reward vs. risk outcomes. A brief walk-through of how a same case would pan out in different, comparable countries:

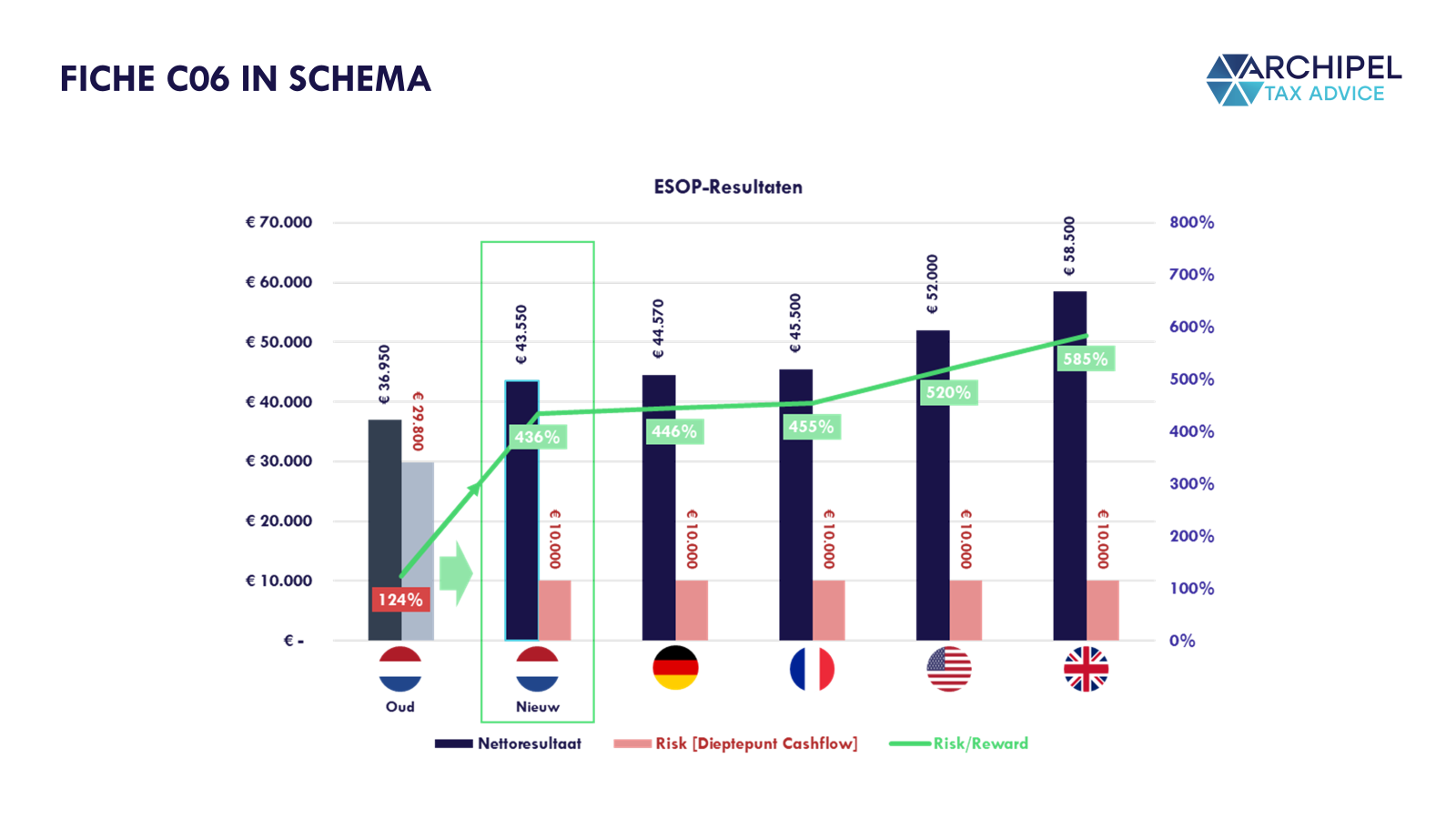

In this example, Felix is granted an ESOPs allowing him to purchase 10% of the company’s equity against a strike price of €10k, aligning with the value the equity pacakge represented when he joined. In year 2, Felix exercises as his ESOP allows, and he pays the €10k strike price to the company and obtains 10% of its stock, then worth €30k. In year 5, his 3-year lockup ends and his benefit is calculated. The 10% stock flight is then worth €50k, and due to a netting clause in the contract, Felix must then pay a 49,5% tax hit on the €40k ‘in the money amount’ – adding another €19,8k to his bill.

From this moment on, the shares are taxed as equity. In year 7, Felix tags along in the exit and sells his 10% stake at €75k, meaning his ‘exit value’ -/- ‘entry value’ gain of €25k is taxed at the 36% equity rate (Box 2). When we deduct these cumulated tax and strike cashouts from his €75k sales proceeds, he ultimately pockets €37k. As his max pre-invested/footed amount was €29,8k, his Reward over Risk ratio is 123,9%.

Were this Germany, France the US or the UK, this rate would have been 446%-588% largely because rates are lower and taxes are later. So: time to make a change.

What the proposal changes (and what it doesn’t)

The central change in the new proposal is that taxation moves to the moment of sale. This aligns tax with liquidity in a way that most ecosystems would consider standard; you realize a gain, you pay the tax. Until then, you do not. Alongside that, the effective tax rate is brought down. The ESOP-benefit remains taxed ‘in Box 1’, so as a wage item, but only 65% of the ESOP gain is taxable, resulting in an effective rate of just over 32% (65%*49,5% max).

The policy rationale here is that when employees choose to work at a ‘qualifying’ startup or scaleup company (more on that later), they accept a risk that is comparable to that of a founder where it pertains to their incentive plan aside fixed wage. This is true only where it pertains to value that they’ve helped build; the value that was already there when they joined, has been created under someone else’s risk ownership. That’s why the proposal grants this discount only from FMV at grant up, and effectively introduces a ‘founder-like’ (Box 2) rate for that part.

Again, it is worth noting that the proposal does not actually move ESOP income into Box 2 or 3; the benefit remains a wage element and should be payrolled as such at tax trigger time (disposal), be it under application of the 35% exemption. This is ‘a matter of technique’ though; early taxation and a high headline rate are largely addressed and a walk-through of Felix’ outcomes under the proposal shows a drastically improved outcome. This the effect of Felix no longer having to ‘foot the tax bill’ and being subjected to a lower rate on the exit:

The Regime’s Scope is Targeted:

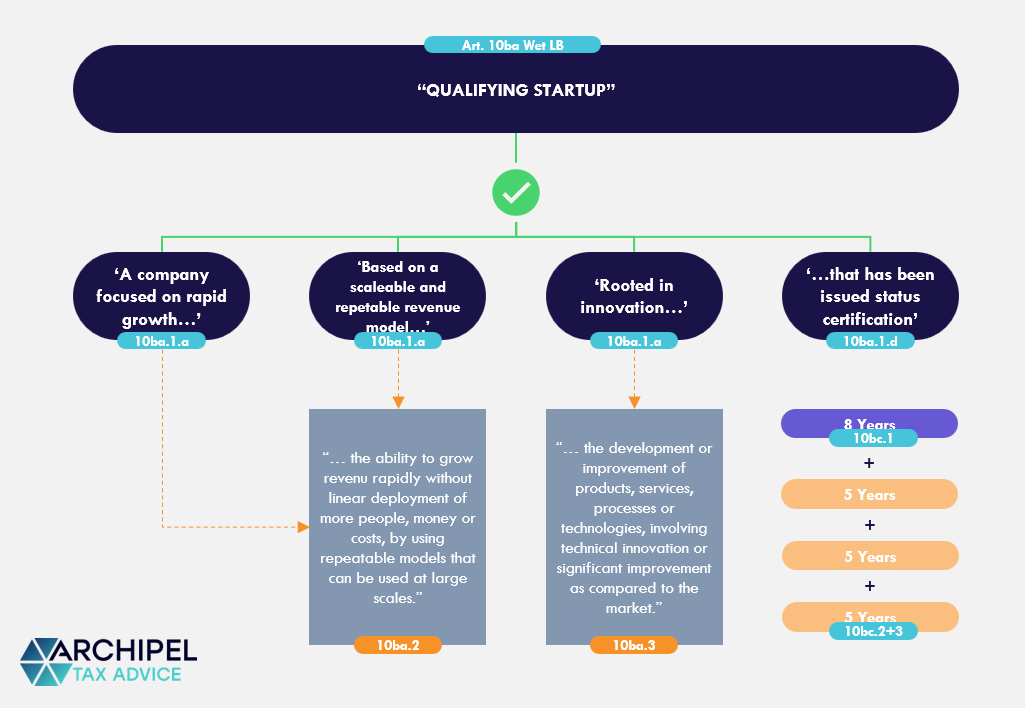

This deferral-and-discount-regime is not generic ESOP tax reform, but rather a tergeted measure to advance certain startup policy goals, which is especially important in light of the Box 3 reform already mentioned. Access is open to companies that meet the criteria of being a ‘qualifying’ startup / scaleup company, and obtain certification on that from the Netherlands Enterprise Agency.

This definition focuses on companies that pursue rapid growth through a scalable model rooted in innovation, while not being listed or part of a listed group. In practice, a combination of funding history and indicators like WBSO eligibility will likely serve as proof points:

That targeting reflects a budget constraint as much as a policy choice. Broad relief would be expensive. By limiting the regime to companies that are both capital-constrained, generally high-growth and low-yield, and policy-relevant, the government keeps the measure contained while still addressing the specific problem it is trying to solve.

Plan design becomes more important

Aside from the company parameters, the proposal also puts more emphasis on how ESOPs are structured. To qualify, plans are expected to include a fair market value strike price, a minimum vesting period and a right of first refusal for the company.

The fair market value requirement ensures that only future value creation benefits from the lower effective rate. The vesting requirement is aimed at avoiding last-minute grants ahead of an exit. And the right of first refusal mainly serves an enforcement purpose, allowing the company (and by extension, the tax authorities) to track when a taxable sale occurs.

Some of these elements, particularly the proposed two-year vesting period, are still under discussion. But the direction is clear: the regime is intended for genuine long-term participation, not for opportunistic structuring.

This sits alongside the box 3 discussion

This ESOP reform is also related to what’s happening in Box 3; the broader shift towards taxing actual returns, including unrealised gains, introduces its own issues for startup investments which, if succesful, produce high growth but low yield for a prolonged time while selling base to cover for the ‘unrealized gains tax’ is often not an option.

The current Box 3 proposal partially addresses this by keeping investments in ‘certified startups’ on a capital gains basis and the startup definition is linked to this ESOP proposal. In effect, the result is that both employees and investors are given a form of deferral: employees through the ESOP regime, investors through the box 3 carve-out. This two-sided approach recognises that talent and capital constraints tend to reinforce each other.

Where this leaves companies today

The legislation is not final yet, and some details will move. Foreseeably particularly those around the definition of a qualifying company and the mechanics of certification. What does seem settled is the direction; the Netherlands is moving to a system where ESOP taxation follows economic realizations more closely, both in timing and in rate. For most venture-backed companies, that removes the need to engineer around the tax system in order to make equity work.

In practical terms, this is not yet the moment for wholesale redesigns of existing plans but it is a good moment to review whether current structures can be aligned with the expected requirements, and to start preparing for certification if the company is likely to fall within scope. The proposed Startup and Scaleup Tax Incentive Act would instate a startup-definition into tax law and impose a favored regime for investments and ESOPs in such growth companies, and these tweaks should make a noticeable difference in the Dutch ecosystem. We are excited to see the bill pass the House and learn what effects it will have!

Want to discuss? Book a slot, it’s on the house!

Feel free to select an easy slot – happy to help!