The rules governing how goods flow from non-EU countries into the European Union are about to change significantly. As of 1 July 2026, the EU will remove the €150 threshold below which imported goods are exempt from customs duties and introduce a €3 fixed customs duty for low-value parcels. Additionally, a handling fee of €2 is expected to be introduced on these parcels from 1 November 2026. For non-EU e-commerce businesses shipping directly to European consumers, this is one of the biggest regulatory shifts in recent years, and it’s time to prepare your business.

Where Things Stand Today

When importing goods into the EU, both VAT and customs duties are generally due at the point of entry. Until July 2021, all goods entering the EU that had a value below €22 were subject to a VAT exemption, resulting in no payable VAT. The €22 VAT exemption for low-value parcels was removed five years ago, and all goods entering the EU have been subject to import-VAT. To ease compliance for non-EU sellers at that time, the EU introduced the Import One-Stop Shop (IOSS), a voluntary scheme that allows sellers to collect VAT at the point of sale, declare it through a single monthly return, and ship goods into the EU without the consumer facing a VAT charge at the door. For B2C shipments with a low value, IOSS has become the standard mechanism for most international e-commerce businesses.

Even though (low-valued) goods are now taxed with import-VAT, there is still a customs duty exemption for shipments valued below €150. Under the current rules, these low-value shipments enter the EU free of customs duties.

What is Changing?

Two important changes take effect on 1 July 2026 with regard to the customs duties. First, the existing €150 customs duty exemption for low-value shipments is removed entirely. Every parcel entering the EU, regardless of its value, will be subject to customs duties from that date onward. Secondly, the EU is introducing a fixed customs duty of €3 per product category on small parcels valued at less than €150 to cover the administrative costs of customs processing. These two measures are have adistinct from the proposed so-called “handling fee” which is currently being discussed in the context of the customs reforms. We expect the €2 handling fee will be introduced in November 2026.

By the end of 2026 we have these three new changes:

- No customs duty exemption for low-value shipments;

- A fixed customs duty of €3 on small parcels valued at less than €150;

- A €2 handling fee on small parcels valued at less than €150.

The above measures do not apply to shipment parcels with a value above €150, the “normal” customs rules are applicable.

How does it work practically between July and November 2026?

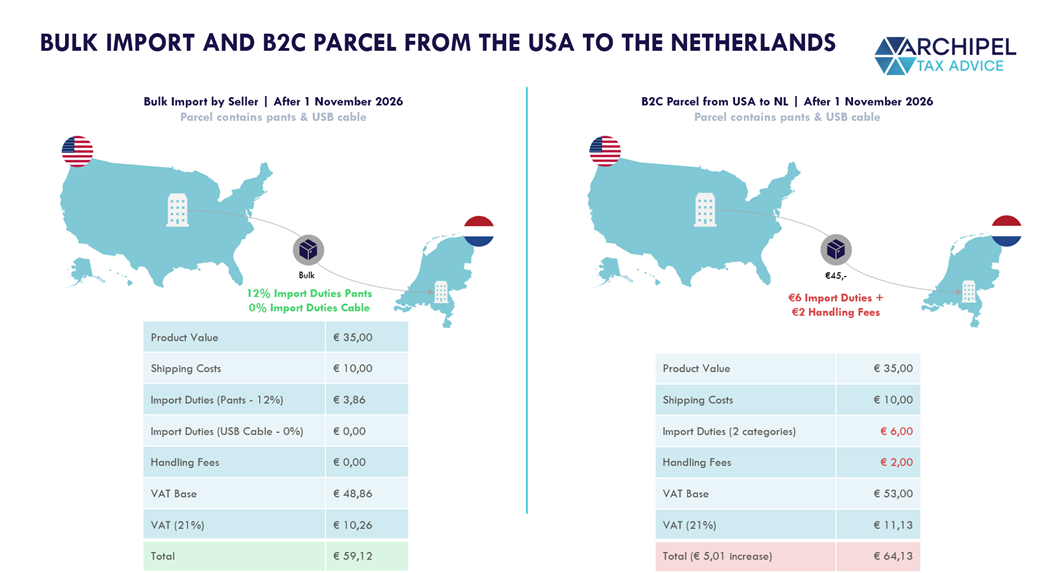

When a consumer, for example, receives a USB cable and a pair of pants in the same parcel with a value below €150, they will have to pay €6 flat-rate customs duties, as these fall into different product categories. Besides the customs charges, VAT is applicable. VAT is calculated on the total value of the shipment; thus, the value of the products and the import duties.

In the visual below, we illustrate the VAT and import duties liabilities on a parcel, containing a pair of pants and a USB cable, being sold by a USA company to a customer in the Netherlands. These import duties apply to all B2C parcels shipped from a non-EU country to the EU.

And how does it work practically from November 2026 onwards?

From November 2026, the €2 handling fee is added on top of the fixed customs duties already in effect since July. Returning to our earlier example of a parcel containing a USB cable and a pair of pants, valued below €150, the charges stack up as follows: a €3 fixed customs duty applies per product category, resulting in €6 for two categories combined. On top of that, the €2 handling fee is charged once per parcel. VAT is then calculated on the full value of the shipment, which includes the product price, the customs duties, and the handling fee.

The visual below illustrates the total VAT and import cost for this same parcel shipped from a USA company to a customer in the Netherlands under the November 2026 rules.

The cumulative impact is significant. Where that same parcel once arrived at a consumer’s door duty-free, with VAT settled at checkout through IOSS, it now carries €8 in fixed charges before VAT is even applied. For businesses shipping high volumes of small parcels, this is a structural cost increase that demands a structural solution.

Summary: July to November 2026, and November 2026 onwards

To help you navigate this regulatory shift, the timeline below outlines exactly how the new customs rules and fees apply to direct B2C shipments valued under €150 entering the EU:

- Before 1 July 2026: Low-value shipments enter the EU free of customs duties under the current exemption rules. Import VAT is applicable, but no additional fixed customs fees are levied at the border.

- From 1 July to 1 November 2026: The €150 customs duty exemption is completely removed. Every parcel becomes subject to customs duties, and a new fixed customs duty of €3 is introduced per product category within a shipment. This fixed duty increases the VAT base, as VAT is calculated on the combined total of the product value, shipping costs, and import duties.

- From 1 November 2026 Onwards: The final measure takes effect with the introduction of a €2 handling fee, charged once per parcel. This handling fee is stacked on top of the €3 fixed customs duties already in place. Consequently, VAT from this date onward is calculated on the full value of the shipment, including the product price, shipping costs, product-category customs duties, and the per-parcel handling fee.

Why is the EU changing this?

The reform is driven by three policy objectives. First, it aims to create a level playing field. EU-based businesses have always been subject to customs duties on their products, whereas non-EU competitors have long benefited from the low-value exemption to offer goods at structurally lower prices.

Second, the unchecked flow of low-value parcels, in particular from Asian marketplaces, has raised concerns about product safety and compliance with EU standards. Removing the threshold gives customs authorities a clearer mandate to inspect goods.

Third, the sheer volume of small parcels arriving in the EU contributes to higher carbon emissions from logistics compared to bulk parcels. The new rules encourage more consolidated shipments resulting in lower emissions from the logistics process.

A Surprise at the Doorstep

If no structured solution is in place, the customs duty and any remaining VAT obligations will be collected from the consumer at delivery, alongside administrative handling fees charged by the courier. This could be a damaging outcome for an e-commerce brand. Customers who ordered a product at a given price, only to be confronted with an unexpected charge before they can receive it, will probably return the parcel or dispute the purchase.

The goal of any compliant structure should therefore be to ensure that all taxes and duties are settled, so that the customer receives their package on a “Delivered Duty Paid” basis, with no surprises.

The Solution: The Dutch Gateway & Fiscal Representation

For non-EU businesses, the most effective response to these changes is not just a fiscal one, it is also a logistical one. Rather than shipping individual parcels directly to consumers across the EU, the smarter approach is to consolidate shipments by importing goods in bulk into the Netherlands, storing them in a local warehouse, and fulfilling EU orders from the Netherlands. This reduces the number of customs entries, eliminates the fixed duty and handling fee exposure on low-value parcels, and gives customers a faster delivery experience. The Netherlands offers a combination of fiscal and customs tools that make it the perfect gateway for this model.

General Fiscal Representation

Any non-EU company can apply for a Dutch VAT number directly. However, to make use of the Article 23 License and benefit from the Dutch VAT deferment scheme, you are required to appoint a Fiscal Representative holding a general permit issued by the Dutch tax authorities. Archipel Tax Advice is able to act as your local “boots on the ground,” handling your registrations and filings. With a Dutch VAT number, you can clear goods in the Netherlands and then distribute them seamlessly to customers across the EU. If you would like to read more about fiscal representation and the Dutch Article 23-license, please see our article:

he visual below illustrates the difference between the two approaches. On the left, the Dutch Gateway model using fiscal representation and an Article 23 License: goods are imported in bulk into the Netherlands, VAT is deferred at the point of entry, customs duties apply to the aggregate shipment value at the applicable tariff rate, and the per-parcel handling fee is removed. On the right, the direct-shipping model as it applies from November 2026: each individual parcel is subject to a €3 fixed customs duty per product category, the €2 handling fee, and VAT applied over the combined total.

Scaling Across Europe with OSS

The EU has been reforming the VAT rules over the past few years. On 1 July 2021, the EU implemented comprehensive e-commerce VAT reforms and replaced the old, local country-specific distance selling thresholds. A single shared EU threshold of €10,000 applies; below this threshold, companies charge local VAT. For example, if you are VAT-registered in the Netherlands, you’ll charge Dutch VAT on EU sales if you do not exceed €10,000 in revenue. Should you exceed the threshold, there is no need to register in all the EU Member States. You may register in all the EU Member States if you prefer, but you can also make use of the so-called “One Stop Shop” in the country of registration (i.e., the Netherlands). All the B2C sales across the entire EU can be reported and paid through a single quarterly electronic return in the Netherlands.

The Dutch tax authorities then distribute the VAT to the respective countries for you. This reduces administrative burdens and eliminates the need for a web of local tax advisors across 27 different EU Member States.

Don’t Wait Until July

The transition in July will be a big change for e-commerce. Businesses that act now to set up their Dutch infrastructure will be able to offer a “business as usual” experience to their customers, while competitors struggle with delayed shipments and higher handling fees.

It is worth noting that the current reform framework is designed as a transitional measure, with a full review anticipated by 2028. The expectation is that by then, a more permanent and potentially broader customs regime will be in place. Businesses that invest now in the right infrastructure with a Dutch VAT number, an Article 23 License, and a local warehousing setup, will be well-positioned regardless of what the post-2028 rules bring.

Ready to secure your spot in the EU market?

Our team specializes in fiscal representation and helping international sellers navigate the Dutch “Gateway to Europe.” Book a time below for a virtual coffee to talk about the best set up for your e-commerce business.