Good news for those in business on the EU-UAE axis: the UAE is no longer considered a ‘low tax jurisdiction’ for Dutch tax purposes following the implementation of Corporate Income Tax in the UAE.

Therefore, in its updated version of the list of low-taxed and non-cooperative jurisdictions 2024 (in Dutch: Regeling laagbelastende staten en niet-coöperatieve rechtsgebieden voor belastingdoeleinden) (‘the Dutch Blacklist’), the Dutch Ministry of Finance removed the United Arab Emirates (‘UAE’). However, Antigua and Barbuda, Belize, Russian Federation and Seychelles were added. The update is effective as of January 1, 2024 and will apply for financial years that start on January 1, 2024 or after.

What is this Dutch ‘Blacklist’ and its impact?

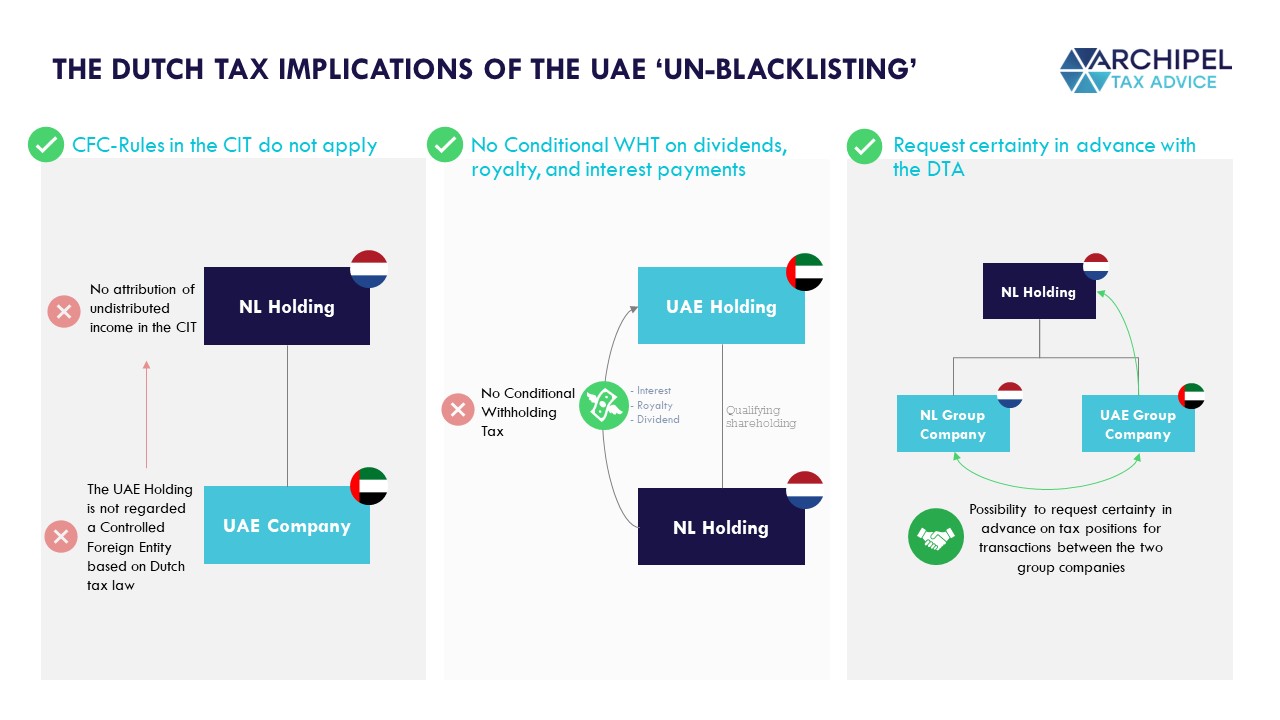

The Dutch List is a generic list of jurisdictions that are considered prone to abusive tax structures as they levy no, or low taxation [<9%]. The list applies to several Dutch tax codes and regulations. As a result, a Dutch-based company that deals with group companies located in blacklisted jurisdictions can face Dutch ‘conditional’ withholding taxes or Dutch corporate income tax consequences on its dealings with taxpayers in said blacklisted states.

Anti-abuse Withholding Taxes on abusive payments made to Blacklisted States

Payments of dividends, royalties and interests that would be deductble from the Dutch taxable base but ‘picked up’ in a low-or-no-tax jurisdiction, would give rise to tax arbitrage and erode the taxable base in the Netherlands / Europe. As an anti-abuse measure, a conditional withholding tax equal to the Dutch CIT rate may be imposed on such payments in abusive situations, eliminating the arbitrage and eradicating the abusive benefit.

No Access to Advance Certainty for dealings with Blacklisted States

Also, certainty in advance from the Dutch Tax Authorities (‘DTA’) cannot be obtained for dealings with group companies in blacklisted jurisdictions (please see more information below under ‘Dutch Tax Implications of the Removal of the UAE from the Dutch List’).

The UAE now meets the Dutch ‘CIT Rate Test’ and is no longer Blacklisted

The Dutch Ministry of Finance removed the UAE from the list as it meets the requirement that companies in the UAE are subject to a tax on profits at a rate of 9% or more. Therefore, the UAE is no longer considered a low-taxed jurisdiction.

In 2023, the UAE has introduced a ‘Corporate Tax Law’ (‘CTL’) for corporations and businesses in the UAE. The introduction was seen as a policy shift as the UAE was known as a zero-tax jurisdiction and therefore attractive for businesses. The UAE Ministry of Finance explains that a competitive Corporate Tax regime based on international best practices is expected to cement the UAE’s position as a leading global hub for business and investment and accelerate the UAE’s development and transformation to achieve its strategic objectives. Companies and corporates located in the UAE will be levied a 0% for taxable income up to AED 375,000 and 9% of the exceeding amount.

Antigua and Barbuda, Belize, Russian Federation and Seychelles are regarded as non-cooperative jurisdictions by the EU and are added to the Blacklist.

Regularly, the EU publishes its list of non-cooperative jurisdictions for tax purposes (‘EU List’). As stated by the European Commission, the EU list consist of jurisdictions that -from an EU-perspective- have failed to fulfil their commitments to comply with Tax Good Governance criteria within a specific timeframe, and jurisdictions which have refused to do so. The EU monitors the measures implemented by jurisdictions to comply with their commitments. The Dutch Ministry of Finance mirrors the EU List to determine which countries would be regarded as non-cooperative as laid out in article 13ab, par. 3, subpart e CITA.

Implications of the Unlisting from the Dutch Tax Blacklist.

The Dutch Blacklist is a generic regulation and is regularly updated by the Dutch Ministry of Finance. Several Dutch tax acts and regulations refer to the Dutch Blacklist, including the following:

- The Dutch Conditional Withholding Tax (‘CWHT’) (in Dutch: Wet Bronbelasting 2021)

- The Dutch Corporate Income Tax (‘CIT’) (in Dutch: Wet op de vennootschapsbelasting 1969)

- Decree on preliminary consultation regarding rulings with an international character (in Dutch: Besluit vooroverleg rulings met een internationaal karakter),

An overview of some of the positive Dutch tax consequences of the removal of the UAE from the Dutch List:

Want to Discuss? Book a Chat with Max!

We are happy to dive in – it’s on the house.